Like the U.S. housing market, Canadian real estate has seen remarkable appreciation over the course of the pandemic, and subsequent affordability concerns were a hot topic during the most recent Canadian election. For Canadians pondering a relocation to the U.S., certain considerations must be analyzed regarding the assets they leave behind. This article focuses specifically on the options associated with Canadian residential real estate through a cross-border lens.

Summary and Takeaways

Canadians considering moving to the U.S. should understand the implications of that move, in terms of the tax liability it can potentially trigger on capital gains. For instance, if you qualify for a Canadian Principal Residence Exemption (PRE) then you may not have to pay the tax on the sale of that home. That’s where Canada’s “Change of Use” and “Deemed Disposition” rules regarding a residence can have a major impact, and either save you tax dollars or result in a tax burden you must pay. All of that is explained in our article, which also points out strategies to minimize or eliminate taxes.

Key Takeaways

- A “Deemed Disposition” occurs when there is a change of use in Canadian real estate, whether it alters from a personal-use residence to a rental property or vice versa.

- If a principal residence were transformed into an income producing property, the Canadian PRE could be reported to nullify the capital gains taxes, as long as specific ownership and Canadian tax residency tests are met.

- However, if a rental property is converted back to personal use, the deemed disposition may result in a taxable capital gain.

- Everyone’s situation is unique, and the sooner you can start planning ahead prior to your move, in order to minimize your taxes, the better.

Canadian Principal Residence Exemption (PRE)

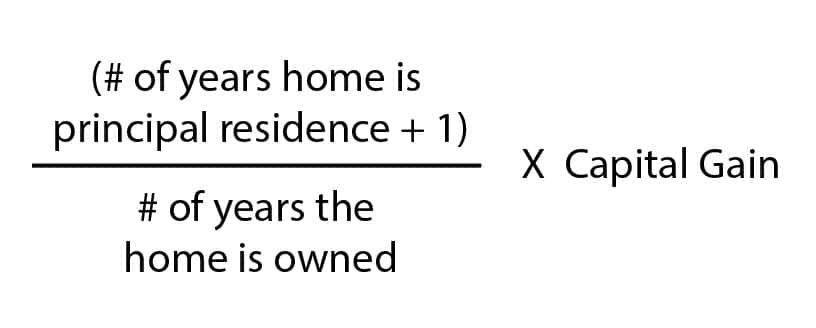

In Canada, current law dictates that the sale of your principal residence does not result in a taxable event—no matter the size of the gain—as long as certain criteria are met. This is one area of the Canadian tax system that is more favorable than its U.S. counterpart. The U.S. allows just $500K (for homeowners who are married and filing joint) of tax-free capital gains upon the sale of one’s principal residence. For the Canadian PRE, the calculation formula is as follows:

If a move to the U.S. were to become a reality, it’s important to recognize how the Canadian PRE is factored. It can provide clarity surrounding critical timelines so as to maximize the exemption. Due to the “+1” in the numerator of the Canadian PRE calculation, Canadians would need to sell their Canadian principal residence within a year of establishing U.S. residency to optimize the Canadian PRE.

For a variety of reasons, some individuals consider converting their Canadian principal residence to a rental property. This “change in use” requires additional action and understanding.

Canadian “Change of Use” Rules for a Principal Residence

A “Deemed Disposition” occurs when there is a change of use in Canadian real estate, whether it alters from a personal-use residence to a rental property or vice versa. This means that the owner is deemed to have sold and immediately repurchased the property even though neither transaction transpired. If a rental property is converted to personal use, the deemed disposition may result in a taxable capital gain. On the other hand, if a principal residence were transformed into an income producing property, the Canadian PRE could be reported to nullify the capital gains taxes, assuming certain ownership and Canadian tax residency tests were met.

S.45(2) Election – Defer Capital Gain Until Property Sold – Change in Use from Personal Use to Rental Property

If a Canadian resident were to file a S. 45(2) Election in the year of the change in use, the change in use would be deemed to have not actually taken place. The benefit here lies in the fact that the PRE could be extended an additional four taxation years, even if the property is no longer inhabited by the taxpayer. These four taxation years could be added to the numerator in the aforementioned PRE calculation, assuming certain criteria are met.

In order to leverage this S. 45(2) Election, certain stipulations would need to be satisfied. For example, the rental property owner could not claim capital cost allowance (CCA) while the election is in force. If the property owner were a non-resident of Canada, the election could still be made. However, he/she would lose the four-year PRE extension. If the election were made, the non-resident owner could still benefit from the deferred capital gain.

In the case of a move to the U.S., it is typically best to let the deemed disposition occur, leveraging the PRE on the unrealized gains, whilst resetting the cost basis for the converted rental property, and therefore matching the cost basis of the property for U.S purposes.

S.45(3) Election – Change in Use from Rental Property to Personal Use

In a scenario absent a S. 45(2) Election, a change in use from income-producing to principal residence would result in a deemed disposition of unrealized capital gains. The recognition of this gain could be deferred if a S. 45(3) Election were filed in the year of the eventual sale of the property. Like the S. 45(2) Election, the S. 45(3) Election has certain stipulations attached, one being that the income producing property did not claim the capital cost allowance (CCA) while it was utilized as a rental property. The S. 45(3) Election can potentially allow the owner to look back four years and designate the rental property as their principal residence if certain criteria are met and the owner is a Canadian resident. For a U.S. owner (non-resident of Canada) of Canadian real estate, the benefit would be reduced to deferment of unrealized gains when utilizing a S. 45(3) Election. Once the property is sold, the deferred capital gain will be realized and accounted for.

Conclusion

Real estate trends in both Canada and the U.S. have resulted in significant appreciation for many of our clients. Relocation from Canada to the U.S. or vice versa prompts careful planning including what to do with real estate left behind on either side of the border. A careful understanding of each individual’s unique circumstances is imperative to maximizing available planning strategies. There truly is no one size that fits all. To further examine your specific cross-border scenario inclusive of your real estate assets, contact Cardinal Point.