Canadians Living in America Resource Hub

The Canadians Living in America Hub is your go-to resource for navigating the complexities of cross-border financial planning. Tailored for Canadians residing in the United States and those contemplating a move across the border, this comprehensive hub offers current advice from knowledgeable cross-border financial advisors and industry experts.

CANADIANS LIVING IN AMERICA RESOURCE HUB

The Canadians Living in America Hub is your go-to resource for navigating the complexities of cross-border financial planning. Tailored for Canadians residing in the United States and those contemplating a move across the border, this comprehensive hub offers current advice from knowledgeable cross-border financial advisors and industry experts.

Delve into our extensive collection of resources, featuring informative blogs, eBooks, videos, infographics, and guidebooks. Each resource provides guidance and insights to assist you in minimizing tax obligations, reducing liabilities, and avoiding filing penalties. Whether you’ve been living here for a while or are considering a relocation, discover the timely, practical insights necessary to effectively manage your cross-border lifestyle.

CANADIANS LIVING IN AMERICA EBOOKS

Our eBooks serve as essential tools for the Canadian community living in America, addressing their specific challenges when adapting to life across borders. These digital guides cover a wide range of topics such as financial planning and regulatory intricacies, aiming to inform and guide readers in making informed choices. Whether it’s understanding tax implications or legal requirements, each eBook explores the complexities in a clear and concise manner. By combining knowledge with user-friendly accessibility, our eBooks equip readers with practical insights to confidently navigate the potential tax and financial pitfalls of cross-border living.

Tax-Efficient Post Secondary School Savings Strategies for Cross-border Families: RESP vs. 529 Plan

Families with cross-border ties—especially those with children studying internationally between the U.S. and Canada—face unique challenges and opportunities when saving for education. Understanding the tax rules, government incentives, and optimal strategies for 529 plans (U.S.) and RESPs (Canada) can maximize the value of your post-secondary savings. Here’s a focused guide to the most tax-efficient strategies [...]

Understanding Your Cross-Border Career: Navigating the Canada-U.S. Totalization Agreement for Pension Benefits Ebook

Discover how to navigate your cross-border career with our detailed eBook, “Understanding the Canada-U.S. Totalization Agreement.” This guide unravels the complex rules around pensions and living requirements for Canadians and Americans with careers that extend over both countries.

Understanding Canadian Tax Obligations for Non-Residents: An Essential Ebook Guide

Are you a non-resident of Canada considering renting or selling your Canadian property? Understanding your tax obligations is crucial. In this eBook, we offer timely insights relevant to individuals dealing with Canadian tax obligations as non-residents. Learn about: Tax consequences of renting out your Canadian principal residence How to reduce or eliminate the 25% Canadian [...]

An Income Tax Comparison – Moving from Ontario to Florida Ebook

Discover the financial benefits of swapping the snowy landscapes of Ontario for the sunny shores of Florida through our insightful eBook, "An Income Tax Comparison - Moving from Ontario to Florida." This timely guide outlines the tax implications of relocating, offering a detailed analysis of the tax rates in both regions and how they impact [...]

Ebook: Canadian Deductibility of 401(K) Contributions and U.S. Deductibility of RRSP Contributions

New Ebook - Canadian Deductibility of 401(K) Contributions and U.S. Deductibility of RRSP Contributions A Canadian working in the U.S. may be offered a 401(k) plan with matching contributions by their employer. The plan will lower U.S. taxable income, but what effect will it have on Canadian taxable income? Are the matching contributions taxable in [...]

Cross-border Canadian Departure Checklist when moving to the U.S. Ebook

Before Canadians become permanent residents of the U.S., it is important to understand and prepare for the significant differences between these countries as to cross-border financial planning. Mistakes and missed deadlines in these matters can be costly. There are many considerations. Some are obvious, but many are not.

CANADIANS LIVING IN AMERICA INFOGRAPHICS

The infographic section in the Canadians Living in America resource hub is created to distill complex cross-border financial planning, investment management, tax planning, and estate planning concepts into concise, digestible, and easily understandable educational visual maps. Through the strategic use of clear graphics, simplified charts, and engaging visuals, these infographics are designed to clarify financial processes and regulations that affect Canadians residing in the U.S. By visually illustrating and connecting the dots, the infographics transform challenging subjects into straightforward, actionable insights. This approach enables individuals to grasp sophisticated financial strategies and make informed decisions regarding their cross-border financial wellbeing.

Infographic: Canadian Expat – Selling Your Principal Residence

For individuals moving from Canada to the U. S. and planning to sell their Canadian home, there are different Canadian and U.S. tax implications. To avoid or minimize tax liability, specific criteria need to be met around the questions of whether tax residency is in Canada or U.S. when the sale occurs and if the home qualifies as a principal residence. If sold while still a Canadian tax resident, a status that can be maintained for a period beyond the moving date, exemptions apply. Additional compliance requirements need to be met when the property is sold by a U.S. tax resident.

CANADIANS LIVING IN AMERICA VIDEOS

Our timely videos in the Canadians Living in America resource hub feature e insights from seasoned professionals well-versed in Canada-U.S. financial, tax, estate, investment, and wealth management domains. Through interactive Q&A formats, viewers gain clarity on regulatory nuances, ensuring informed decision-making. These strategically selected resources provide Canadian expats with practical strategies for navigating the complexities of the American financial system.

How U.S. Estate Tax Applies to Canadians with U.S. Stocks, ETFs

Cardinal Point’s Terry Ritchie continues his talk with Rob Carrick about U.S. estate taxes; this segment focuses on what they mean to Canadians who own U.S. stocks and ETFs. U.S. shares owned by Canadians are considered U.S. cited, and there could be U.S. estate tax filing requirements if they are valued at more than $60K […]

What Snowbirds Need to Know about U.S. Estate Tax

Cardinal Point’s Terry F. Ritchie talks to Rob Carrick about the latest changes in U.S. estate taxes and what they mean for Canadian snowbirds who own property in the U.S. For many years, snowbirds had to worry about U.S. estate taxes, but it’s not an issue for most anymore, as the threshold is much higher […]

CANADIANS LIVING IN AMERICA BLOGS

Our collection of timely articles authored by seasoned cross-border financial advisors, offers real-world experiences, examples, cautions, strategies, and tactics. Tailored to Canadians residing in America, articles assist in providing guidance for managing cross-border investments, taxes, retirement planning, estate considerations, and comprehensive financial planning. Whether one is working, retiring, spending time in both countries, or earning income across borders, readers can gain invaluable insights into the complexities, rules and regulations of expat finances when living in America.

Moving from Canada to the U.S.: What to do with your Canadian dollar investments

Anyone planning to move from Canada to the United States, or who has already made that move, must give careful consideration to how they manage their Canadian dollar denominated investments. Otherwise they risk consequences such as having those investment accounts frozen or discovering that their Canadian-based financial professionals are prohibited from managing their investments once they become U.S. residents. But to make matters even more complicated, they may be unable to find a qualified financial and tax advisor in the United States to manage their Canadian dollar assets. The good news is that you have viable options and excellent solutions to help you avoid these and other unwanted and costly scenarios. All of that is explained in this highly informative and helpful blog.

U.S. Retirement Healthcare Coverage Options: 2024 Guide

One of the biggest and most important expenses in retirement is health care. Unfortunately, those who don’t plan ahead for adequate health insurance coverage can face tremendous costs and obstacles that can undermine a successful retirement. This article helps to inform those looking forward to retirement about their four main Medicare coverage options, as well as the availability of Medicaid. Additionally, it explains Medigap supplemental insurance, employer-sponsored healthcare insurance plans for retirees, the multiple tax advantages of Health Savings Accounts, and various types of Long Term Care insurance. That information can empower you to make more informed and strategic decisions, based on uniquely individual factors such as your age, net worth, and medical history.

Navigating RRSPs/RRIFs/LIRAs/LIFs: Tax Planning for Canadians Moving to the U.S.

If you are planning to relocate from Canada to the United States, you will still want to hold on to the wealth potential of Canadian investment accounts. But there are special considerations and tax planning strategies for those who have Registered Retirement Savings Plans, Registered Retirement Income Funds, Locked-In Retirement Accounts, and/or Life Income Funds. This insightful article provides an overview of the applicable rules and regulations along with key strategies for optimizing your tax and wealth management planning. It also describes the kind of tax reporting that may be mandatory to ensure full compliance with the laws of both Canada and the U.S.

US Taxation of Your Canadian Rental Home

For Canadians moving to the U.S., the options for their home are to sell it, to keep it as a secondary residence, or to rent it. Each has its pros and cons.

Choosing to rent creates tax and capital gains issues in Canada and in the U.S., ongoing tax filing requirements, and the need for a dependable local property manager. Decisions need to be made in a timely way to maximize available tax exemptions. It is complicated, but it may be a wise choice. Cardinal Point’s cross-border specialists can help you decide if it is right for your specific situation and then show you how to use the Canada/U.S. Tax Treaty provisions to your advantage.

Deemed Departure Tax Canada

For Canadian tax residents moving to another country, the Canadian Deemed Departure Tax has significant and complex ramifications that should be carefully considered. Advice in advance of a move from a qualified cross-border tax specialist and financial planner can reveal strategies to best prepare yourself for this tax, including possible exemptions and deferrals.

Selling or Renting Your Canadian Home: Tips for Non-Residents

If you’re a non-resident of Canada but are planning to rent out or sell a home you own within the country, you’ll face certain tax consequences. In this blog post, we’ll take a look at the most common tax obligations associated with both rental and sale of a Canadian principal residence.

Canadian Cross-Border Real Estate Use Rules

When our clients move from Canada to the U.S. or vice versa, they often leave real estate behind. While some choose to sell their former residence, others want to convert it into a rental property. Whichever action they take, tax considerations must be made. Learn more about the Canadian ‘change of use’ rules that should influence these decisions in this article.

Cross-Border Canadian Departure Checklist: Moving to the U.S.

Canadians become permanent residents of the U.S. for many personal and professional reasons. Prior to a move, it’s important to be organized and understand that significant differences exist between Canada and the U.S. when it comes to cross-border financial planning and investment matters. The following actionable items should be considered when cross-border transition planning from […]

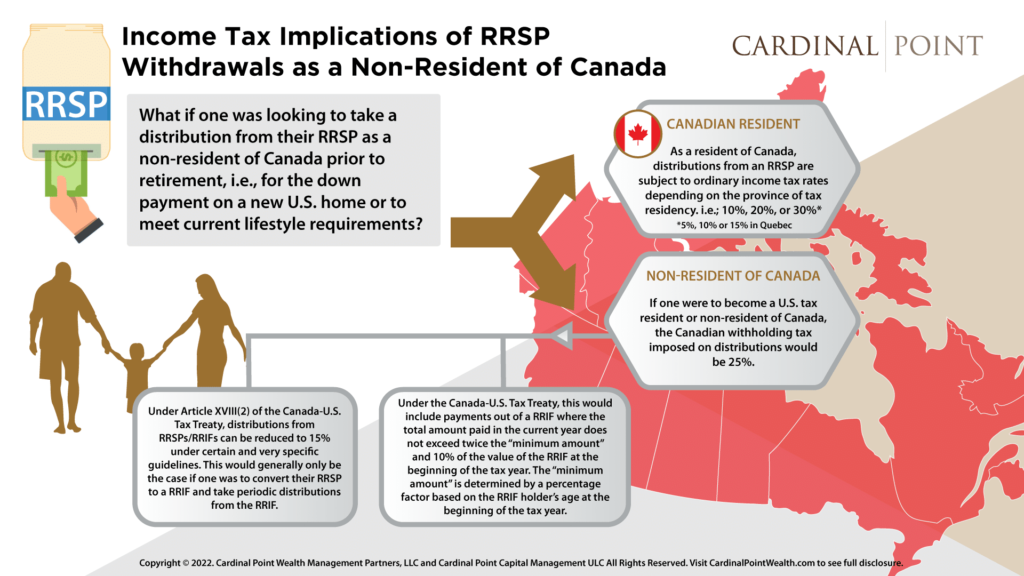

RRSP Withdrawal Tax Implications for Non-Residents

A large number of the clients that we work with are those that move from Canada to the United States. In these cases, we spend quite a bit of time making our clients aware of the income tax implications of leaving Canada and establishing tax residency in the U.S. We have written many publications on […]

Am I a U.S. tax resident?

Most Canadians who move to the U.S. have a good understanding of their immigration residency status. However, many do struggle to determine their residency status for U.S. income tax purposes. While it is common knowledge that U.S. citizens and green card holders are responsible for filing U.S. tax returns, most people who move to the […]