It’s common to hear about the long-term investment averages that we’ve all become accustomed to. Conventional wisdom says that over the long run stocks should earn something like 10% per year. And in that regard, the conventional wisdom is actually pretty good. Over the last 30 years through the end of 2017, the annualized return on the S&P 500 was 10.7%, and 9.0% on the S&P/TSX 60. Given great average annual returns on both markets, financial planning should be a piece of cake right?

Ah, but we know we don’t get that 10% every single year, right? It’s not like a bank savings account that pays out a steady interest stream every month. Some years are better, others are worse. This variability gives rise to measures such as standard deviation, a calculation that tries to paint a picture of how much volatility you will experience in an average year. For the two indexes, the standard deviations have been extremely close over that same 30-year time period; 14.0% on the S&P 500, and 14.1% for the S&P/TSX 60.

That means that for US stocks, in about two thirds of the years, we should experience a return of somewhere between -3% and +25%, if history is a good predictor of the future. In Canada that would mean a range of -5% to +23%.

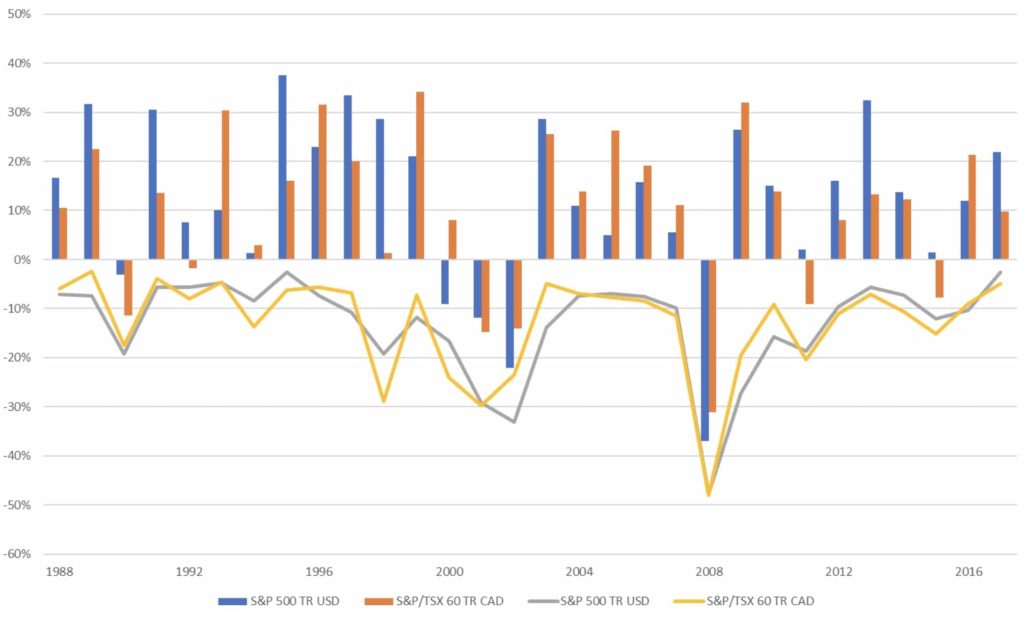

Those seem like reasonable ranges for most years, however we know it’s the years that fall outside of those ranges that we tend to remember. When we look back on returns its easy to remember the boom times of the late 90s, for example 1996 when US stocks gained 23% and Canadian stocks were up 32%. It’s also impossible to forget some of the bad times, like 2008 when US stocks dropped 37% and Canadian stocks fell by 31%.

Yet what’s often lost in these long-term averages and outlier events to the good or bad side, is that year to year we actually see much more variation than you might think by just looking at the end of year numbers. Going back over that same 30 year period, the average intra year decline seen in both the US and Canada was about 13%. That means that on average, at some point during a calendar year, the stock market was in a correction phase- a decline of more than 10% from its high for the year. The chart below show the annual gains since 1988 for both the S&P 500 and the S&P/TSX 60 in blue and red bars, respectively. Below, the line graph shows the largest intra year decline for each year.

Annual Returns and Max Drawdowns

S&P 500 & S&P/TSX 60, 1988-2017

2017 was noteworthy for having a slow and steady gain throughout the year. At no time in the US or Canada did we see markets fall by more than 5% from their previous highs. In fact, as you can see on the chart, going back to 2011, most of the years have seen smaller intra year declines than the average over the entire period.

Losses in a portfolio are never going to feel good. However, we should put the current losses into context. The recent volatility we’ve seen, with drops between 5% and 10%, is not only completely normal, but still below average for intra year market movements. In fact, it’s this uncertainly, or risk, that is a real part of why we expect higher returns in stocks than safer investments like bonds, CDs or GICs.

Also, it’s important to keep in mind that these volatile movements in the stock market are only one part of a diversified portfolio. By combining stocks in the US, Canada and the rest of the world with less volatile bonds, your allocation can be tailored to meet your investing needs.

Persevering through the short-term ups and downs are part of the price investors must pay to capture those long-term higher rates of return. Ensuring that you have the right amount of those less volatile components in a portfolio can help you stick to the long term plan you’ve set in place.

Source: Morningstar Direct 2018. Indexes are unmanaged baskets of securities that are not available for direct investment by investors. Index performance does not reflect the expenses associated with the management of an actual portfolio. Past performance is not a guarantee of future results. Foreign securities involve additional risks, including foreign currency changes, political risks, foreign taxes, and different methods of accounting and financial reporting. All investments involve risk, including the loss of principal and cannot be guaranteed against loss by a bank, custodian, or any other financial institution.