Diversification is the most important concept in investing, but also perhaps the least exciting. If anyone knew for sure exactly which one company or country would have the highest return in the coming year, there would be no reason to hold anything else. But while being able to predict markets with any certainty sounds great in theory, in practice nobody has been able to consistently outsmart the market. So what do you do if you can’t know for sure if Pepsi or Coke, or the US or Canada will be the best performer in the coming year? You diversify. This is especially important when it comes to financial planning.

While we may plan to retire in one country or have our peak earnings years in another, having broad-based global diversification can help you over the long run, even though in any give year or time period it can feel like it’s not benefiting you.

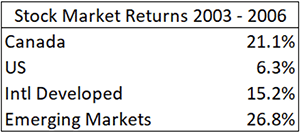

Let’s take an example of a Canadian investor who had a CAD account and was watching returns in the early 2000s. Between the start of 2003 and the end of 2006, the Canadian market far outpaced the US. You can see from the chart on the left that the annualized returns (in CAD) for Canadian markets was nearly triple the returns for US markets over that period.

Let’s take an example of a Canadian investor who had a CAD account and was watching returns in the early 2000s. Between the start of 2003 and the end of 2006, the Canadian market far outpaced the US. You can see from the chart on the left that the annualized returns (in CAD) for Canadian markets was nearly triple the returns for US markets over that period.

Besides Emerging Markets, it would have been hard to see much reason to allocate any investments outside of Canada. And in fact, that’s much of what the Canadian and US investing media was telling you at the time- dump your US stocks, and buy Canadian and Emerging Markets! Yet moving to those markets solely and out of the US and International Developed markets would have been particularly painful shortly after in 2008, when Canadian and Emerging Markets holdings would have underperformed compared to US markets, when viewed in CAD.

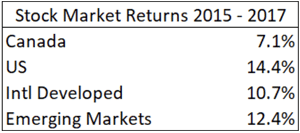

More recently, if we look at 2015-2017, Canada has delivered just half the performance of the US on an annualized basis, and well below the returns experienced in International Developed and Emerging Markets.

More recently, if we look at 2015-2017, Canada has delivered just half the performance of the US on an annualized basis, and well below the returns experienced in International Developed and Emerging Markets.

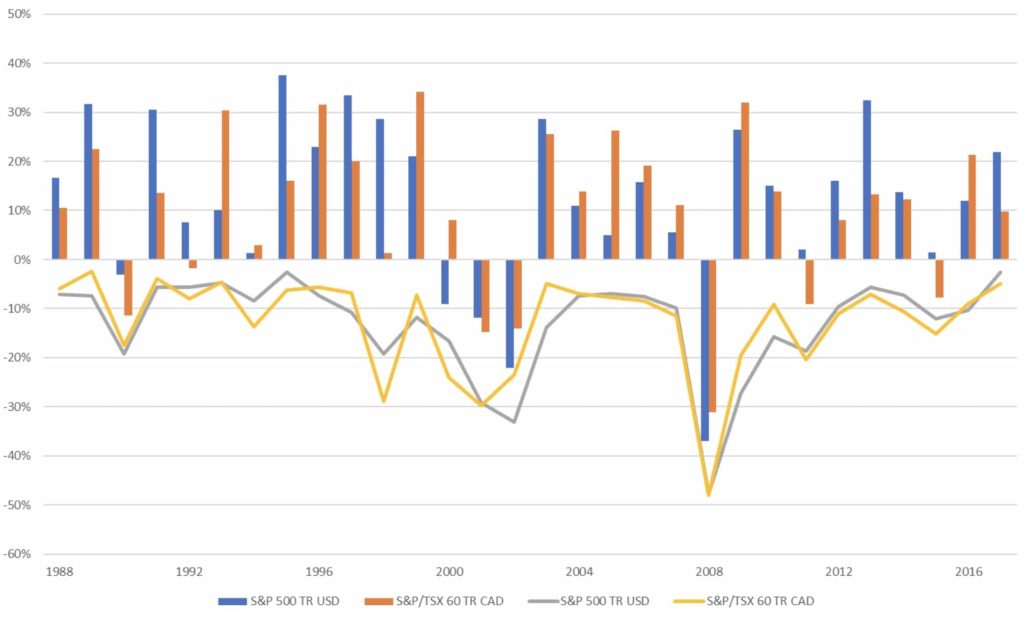

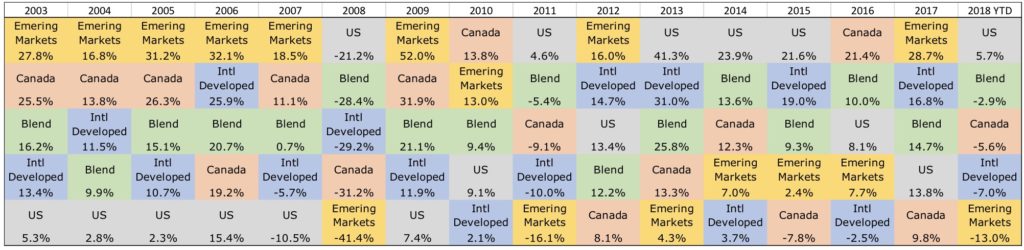

As we can see on the chart below, the order of returns by region each year is essentially random. Trying to guess in advance each year which country or market segment will outperform will likely lead to simply buying what’s been hot in the last year and will often result in disappointment. One area might do well for a number of years, as Emerging Markets did in the early 2000s, only to fall hard in 2008. US stocks did much better than Canadian stocks for 6 of the previous 7 calendar years, but underperformed significantly in 2016, and have experienced steeper declines this October.

Returns by Region

*2018 YTD is Jan 1 – Oct 27

Instead of guessing which country or region is going to outperform next, astute investors can realize many benefits by spreading their assets across the group of global stocks. Doing so allows you to capture the returns of whichever market is doing best in that time period, and ensures you’re never exposed to just one market or currency. As you can see on the chart, a blended exposure to the different regions means you can reduce your year to year volatility, and this is before the introduction of bonds or other asset classes that may move differently than stocks.

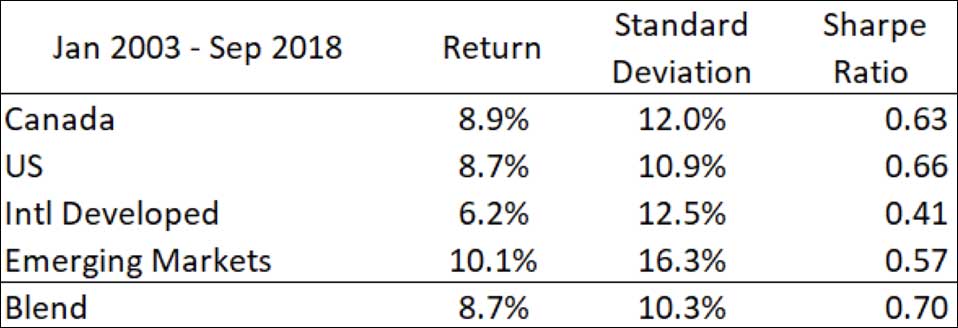

Over the last 15+ years, each region we looked at had strongly positive returns. Standard deviation measures how much those investments went up or down over the years, with Emerging Markets being the most volatile. The Sharpe Ratio measures how efficient each investment was by comparing the magnitude of the returns to the amount of volatility experienced. US stocks looked pretty good during this time period, but they don’t beat the blend when it comes to reward per unit of risk.

Looking back to the chart of annual returns above, we can’t know what region will have the strongest returns over the coming week, month or year. Yet, when we look at the blended result, which made no predictions at all but simply followed a long-term asset allocation between the four regions, we saw the lowest volatility and a healthy return , resulting in the highest Sharpe ratio. This indicates that the blended portfolio is a more efficient stock allocation than holding any one region individually. This blog looked at these regions from the Canadian Dollar point of view, but the results and theory are similar from the US Dollar perspective.

The downside of diversification is that you will never be the best performer. There will always be some particular stock or area of the market that will do better than the whole of your portfolio. But by having a globally diversified portfolio, you’re likely going to be capturing some of those gains. At some points, like 2008 or recently in 2018, all markets may see losses, however diversification ensures that you’re not taking unnecessary risk by having all of your exposure in any one company, sector, or country.

Thinking back to the financial plan that is crucial to the ability to meet long term goals, the long-term growth rates assumed are already factoring in ups and downs along the way. Nowhere in a prudent investment plan is the need to try and predict or out guess markets, but key to the plan is being able to capture those market rates of return wherever and whenever they do occur.

Source: Morningstar Direct 2018. Canada returns represented by S&P/TSX 60 TR CAD, US returns represented by S&P 500 TR CAD, International Developed represented by MSCI EAFE NR CAD, Emerging Markets represented by MSCI EM GR CAD. Blended mix represents 33% in Canada, 33% in US, 23% in Intl Developed and 10% in Emerging Markets, rebalanced annually. Indexes are unmanaged baskets of securities that are not available for direct investment by investors. Index performance does not reflect the expenses associated with the management of an actual portfolio. Past performance is not a guarantee of future results. Foreign securities involve additional risks, including foreign currency changes, political risks, foreign taxes, and different methods of accounting and financial reporting. All investments involve risk, including the loss of principal and cannot be guaranteed against loss by a bank, custodian, or any other financial institution