A Wall Street Journal article a few weeks ago cautioned investors about the hidden risks in bonds. It has been a recurring headline we’ve noticed the last few months, particularly as yields on the US Treasury 10-year bond have increased from below 1% to about 1.60% currently. With economic activity and inflationary forces poised to rise this year, how much of a concern should investors have over their bond holdings?

Summary and Takeaways

The current economy is rather unpredictable, and interest rates are rising. That’s why many investors wonder about the potential risk that bonds may represent. But headlines about bond risk should not cause undue worry. During almost any year you examine, the bond market overall tends to exhibit fairly low volatility. Bonds can also play an important role as ballast within your financial portfolio to keep it on a more even keel.

Key Takeaways

- The total return on bonds is a combination of the current yield and any capital gains or losses on the principal value of the bond.

- One way to mitigate risk in the bond market is to avoid exposure to those that represent credit risk – although such junk bonds may offer higher yields. Bonds with especially long maturation periods can also carry significant interest rate risks.

- The bond portion of an investment account may experience challenges, but its goal and role should stay the same – to provide a steady stream of returns and act to counterbalance to the inevitable ups and downs of the stock market.

- Over time and historically, bonds that are carefully and strategically selected based on your unique investment goals can add stability to your portfolio – even through tumultuous markets.

Rising yields do put a damper on the prices of previously issued bonds. If the prevailing interest rate is higher than those previously issued (and fixed) bond coupons, investors will pay less for those bonds in order for the total yield to be equal rather buying a brand-new bond at a higher rate or an older bond at a lower rate. In recent years like 2019 and 2020 when interest rates were falling, this was a benefit to bond holders who likely saw positive returns in the high-single digit range even as yields headed below 1%.

Total returns on bonds will be the combination of the current yield (the coupon divided by the price you paid for the bond) plus any capital gain or loss on the principal value of the bond. Over the last few decades, bond holders have generally benefited from positive capital gains as yields have fallen. As yields rise, any capital loss has the potential to reduce or even turn the total return negative.

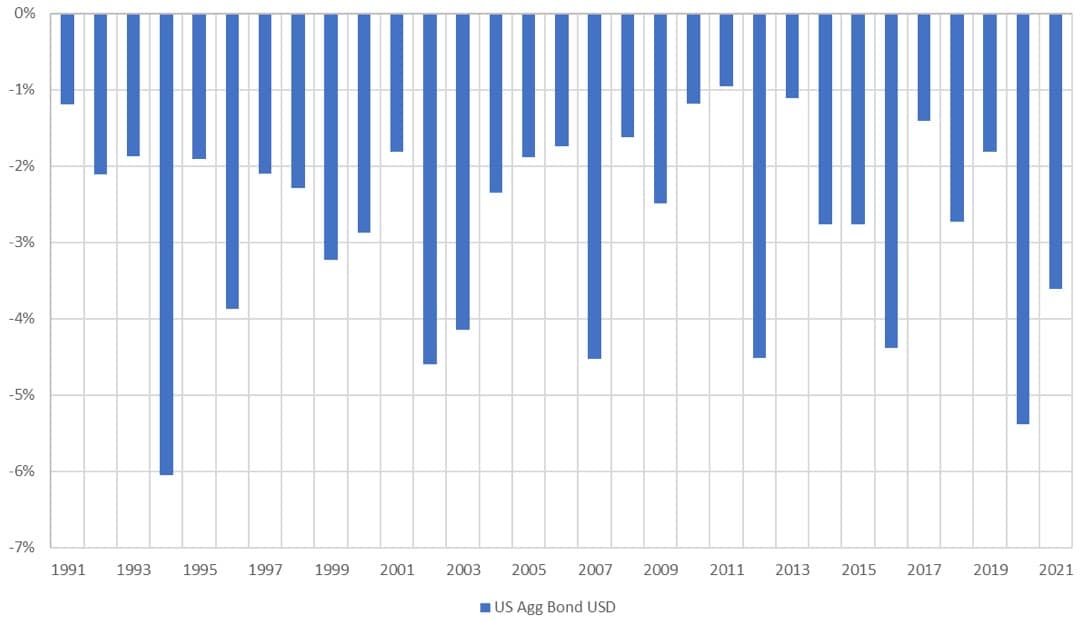

Below we can see the experience of max drawdowns (the most that the investment fell at any point during the year) over the last 30 years for the Barclay’s Bloomberg Aggregate Bond Index—a representation of the entire bond market. A few aspects stick out. During almost every year, we see a drawdown at some point during the year of about 2% or more. However, very rarely, in only two of the 30 plus years, did we see drawdowns of over 5%. This illustration is meant to show that the bond market overall tends to have fairly low volatility.

Maximum Drawdown in Bonds

Weekly, January 1991 – April 2021

Certain elements of the bond market may themselves have much larger exposures to different risks. Credit risk is extremely present in high yield, or junk bonds, and that can be seen by their significant declines in years when stocks are also meaningfully down, like 2008. High yield bonds declined in value by nearly 25% that year.

Bonds with significantly longer maturities, as measured by a duration, can also have significant interest rate risks. For example, in 2013 when the Federal Reserve was just hinting at starting to taper off their bond purchases following the recession of 2008 and the bond market experienced a ‘taper tantrum,’ long-term Government bonds declined by 13% for the year.

When we look at the overall bond market during years such as 2008 or 2013, we observed one slightly positive return and one slightly negative. Both are far away from the excesses of individual parts of the bond market.

At Cardinal Point, as detailed in every client’s Investment Policy Statement, we have long viewed the bond portion of an account as an area that can provide stability as its primary role. The yield and total return are helpful to an overall portfolio, but that must not come at a detriment to that portion of an account’s ability to preserve value when other areas are in distress, as we saw in spring of 2020. We utilize a variety of indexed and actively managed positions to have a dynamic exposure to the fixed income world and, on average, tend to hold bonds with a higher credit quality and a shorter duration than the overall Aggregate Bond Index.

When we see headlines about bond risks, we need to have the background and context that the risk in most investors’ overall bond portfolios is significantly less than the stock portion of their accounts. From January 1st – April 25th of this year, with interest rates increasing by over a half a percent, the total loss reported on the Aggregate Bond Index was only -2.5%. While not an ideal way to start the year, in comparison, stock indexes have the potential to lose 2.5% in one day. Additionally, certain active Bond Managers have been able to limit their interest rate sensitivity, and shorter duration indexes have experienced even smaller loses during the same time period. Taking this into account, bonds are not likely the largest element of short-term risk to consider in your portfolio. Conversely, should yields remain at this level over a longer period of time, investors may look to re-evaluate the portion of their portfolio dedicated to this asset class.

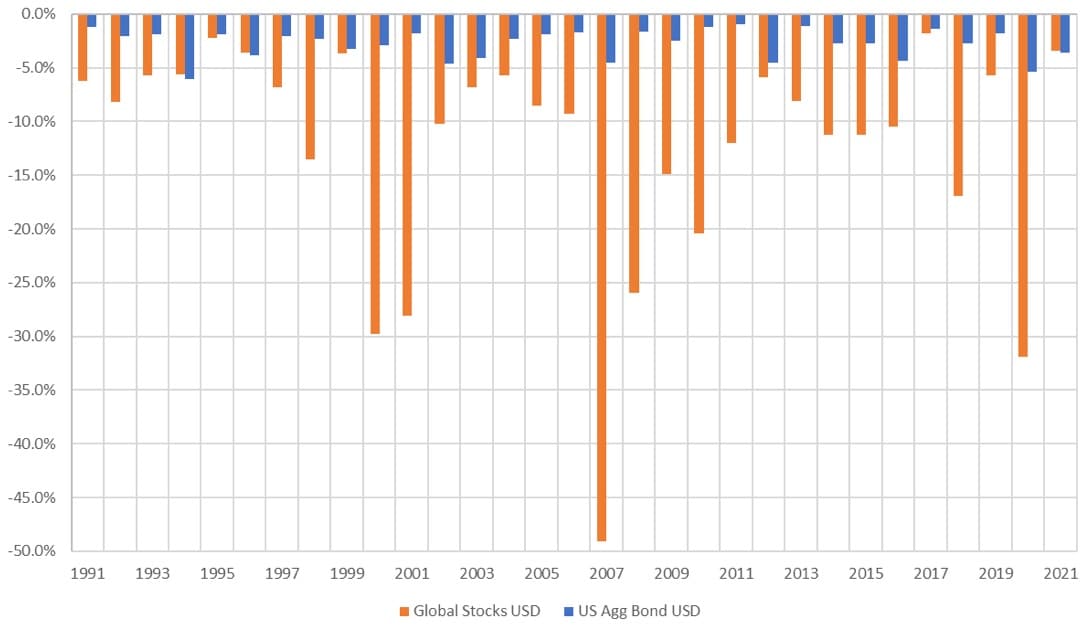

As a comparison below, we have added in the maximum drawdown for a global stock market index over the same time. Here you can see that in virtually every year the drawdowns experienced in stocks dwarf those seen in bonds. Looking at a global stock market exposure, we have seen double-digit drawdowns in nearly half of the years, with nearly one sixth of those years seeing declines of greater than 25%.

Maximum Drawdown in Stocks and Bonds

Weekly, January 1991 – April 2021

The bond portion of investment accounts may present a challenge in the coming years, however, the goal remains the same: to provide a return stream which allows investors to persevere through the inevitable swings of stock markets, while helping to meet the goals of the invested assets.

Indexes used: Bonds- Bloomberg Barclays US Aggregate Bond TR USD, Global Stocks- MSCI World NR USD. Sources: Morningstar Direct 2020, WSJ, As Yields Rise, Beware the Hidden Risks in Ultralong Bonds, Jon Sindreu February 26, 2021

Indexes are unmanaged baskets of securities that are not available for direct investment by investors. Index performance does not reflect the expenses associated with the management of an actual portfolio. Past performance is not a guarantee of future results. Foreign securities involve additional risks, including foreign currency changes, political risks, foreign taxes, and different methods of accounting and financial reporting. Emerging markets involve additional risks, including, but not limited to, currency fluctuation, political instability, foreign taxes, and different methods of accounting and financial reporting. All investments involve risk, including the loss of principal and cannot be guaranteed against loss by a bank, custodian, or any other financial institution.