The strong U.S. dollar has created new challenges for those moving to the United States from Canada. But understanding these challenges and your options can help you more smoothly navigate the financial transition.

Here’s the background. The Canadian dollar has been valued within the same limited range for nearly a decade, and is currently valued between 0.70 and 0.80 against the U.S. dollar. That is big departure from the summer of 2014, when the ratio was 0.90 to 0.95.

In the past, when the currencies were so closely valued, many individuals planning a move to the U.S. elected to convert their bank and non-registered (taxable) investment-account funds to U.S. dollars. After all, it makes sense to hold most of your liquid net worth in your local currency. Also, converting Canadian dollars to U.S. dollars and moving Canadian taxable investment accounts to the United States simplifies tax and foreign-account reporting requirements. It also provides you with better investment opportunities, including those that are more tax efficient – while simplifying your financial and estate planning.

But a Canadian dollar below 0.80 complicates things, as most people are reluctant to convert funds at such a sizeable discount. So, let’s look at options available to individuals or families who do not want to convert their CAD taxable investment accounts to U.S. dollars.

OPTION 1 (which is never ideal): Leave your Canadian investment accounts in Canada.

If you work with a Canadian financial advisor, chances are that adviser is not registered to provide investment or financial planning advice to a U.S. resident.

A financial advisor must always be licensed in the jurisdiction in which a client lives, regardless of the client’s citizenship status or the country in which the assets reside. Thus, once you become a resident of the United States and ask your advisor to update your mailing address on file to your new U.S. address (never leave your old Canadian address on file: see this related article to learn why), one of three things will likely happen:

- Your advisor will inform you that they are no longer able to provide investment advisory services to you and that you must work with someone in the U.S.

- Your advisor will explain that you can keep your accounts on the Canadian platform but that they will be frozen and no further trading or rebalancing can take place.

Your advisor will explain that they are, indeed, registered in the United States and can continue to oversee all investment management services in your accounts.

To reiterate, most Canadian advisors are not registered in the United States. So, your most likely scenarios are Options 1 and 2. In the event that your advisor fits the third scenario, you want to ensure that their services and expertise extend beyond merely providing investment management.

For example, when moving to, and/or living in the United States, clients face a host of cross-border planning complexities. A true cross-border advisor will help construct an integrated Canada-U.S. cross-border financial plan that addresses tax and estate planning matters in addition to the management of your investment assets. It is critically important to align yourself with a firm that boasts a team of seasoned professionals who have earned both Canadian and U.S. credentials and designations. Those include (but aren’t limited to) Canadian CFP, U.S. CFP, Canadian CPA, U.S. CPA, and Chartered Financial Securities Analysts licensed in both Canada and the U.S.

Now, if you do decide to leave your Canadian non-registered accounts in Canada, there are number of important points to consider, such as:

- Drawbacks of Canadian Funds

Canadian-traded mutual funds are considered “not registered for sale” to U.S. residents. Even more importantly, Canadian-traded mutual funds and ETFs are likely categorized as Passive Foreign Investment Companies (PFIC). The earnings and dividends distributed by such investment vehicles are subject to the highest marginal tax rates on your U.S. income tax returns. Holding these securities could also invite additional and more costly U.S. tax filing requirements. (Download our whitepaper on PFICs for further information.)

- Accounting Hurdles

Canadian custodians have a reputation for doing a poor job of complying with U.S. tax reporting requirements. For example, many do not prepare and submit annual U.S. 1099 tax reports showing dividends, interest, and long-term versus short-term capital gains. But these reports are required by law if you are a U.S. resident. Furthermore, many of the tax reporting forms Canadian custodians provide to U.S. resident clients are denominated in Canadian dollars. That means that you or your accountant must convert all taxable and reportable transactions to U.S. dollars before filing your U.S. tax returns. This additional work by can increase the likelihood of errors and lead to significantly more time-consuming and expensive accounting and tax-preparation.

- The Conversion Window

If converting your funds to U.S. dollars once the exchange rate improves is still your goal, make sure your investment strategy is flexible enough to accommodate a future currency conversion. For example, you do not want to be locked into investment products that must be held for a certain period of time. If they are locked when exchange rates improve, you may miss your chance to take advantage and convert because your funds aren’t accessible. Also, make sure your investment accounts are not invested in volatile or speculative securities that are subject to sharp market swings. It would be unfortunate if the exchange rates became attractive but the value of your Canadian-dollar investment holdings had deteriorated due to poor market performance or downside volatility.

- Tax-Aware Investing

Make sure your advisor is managing your account under an investment mandate that reflects your U.S. tax residency. As previously mentioned, U.S. residents are subject to long-term and short-term capital gains tax rates. If you sell an asset that has been held for one year or less, any profit is considered a short-term capital gain, and is taxed at your ordinary income rate (up to 40.8%). If you sell an asset held longer than one year, any profit you make is considered a long-term capital gain, and is typically taxed at a considerably lower rate (15% or 20%). But in Canada, there is no such thing as long-term or short-term capital gains. Canada has just one capital gains rate, and Canadian portfolio managers are trained to oversee client accounts while applying that rate. Also, there are different types of investment securities, such as Canadian preferred shares, that are attractive investments from a Canadian tax standpoint but not from a U.S. tax standpoint. Tax residents of the U.S. should also seek to invest in securities that distribute qualified dividends that are taxed at a more favorable rate than ordinary dividends. For these reasons and others, it is always in your best interest to confirm that the Canadian money manager or advisor has a depth of experience working with U.S. tax residents. Be sure they know how to strategically and effectively customize the management of your portfolio to ensure total compliance with U.S. tax rules.

- Reporting Requirements

You will be subject to extra foreign account reporting requirements by the Internal Revenue Service. Because these accounts are domiciled outside of the United States, the IRS will require you to report specific information about them (account number, highest market value in the tax year, etc.) on a form called the FinCEN Report 114. Additionally, you may have to file an IRS Form 8938 – Statement of Specified Foreign Financial Assets as part of your Form 1040 filing. These increased reporting requirements are time-consuming and will likely lead to substantially higher tax preparation costs.

Once you become a U.S. resident, leaving your Canadian-dollar taxable or non-registered accounts in Canada can be done under limited scenarios. But in light of the considerations above, it certainly is not ideal.

Option 2 (better, but still challenging): Move your Canadian Investment Account to the U.S.

Moving your Canadian-dollar investment accounts to the United States will simplify financial and estate-planning initiatives, and will streamline U.S. tax reporting. But you will still face challenges. For one, most U.S.-based financial advisors will automatically want you to convert your Canadian-dollar accounts to U.S.-dollar accounts − which obviously contradicts your goal of maintaining your holdings in Canadian dollars. The main reason why U.S.-based advisors make this recommendation is that their firm, or its custodian, does not offer multi-currency accounts. The U.S. dollar is the only currency option they are able to provide for your investments. It is rare for U.S. investment firms to offer Canadian dollar-denominated accounts because there is little demand for them in the United States.

Another critical consideration is that investment advisors who do offer multi-currency accounts may not know the Canadian investment market well enough to construct a proper investment portfolio. It is one thing to be able to open a Canadian-dollar-denominated account on behalf of a client (which as mentioned above, is rare). But it is quite a different matter for a financial advisor or portfolio manager to have the knowledge base, experienced acumen, and extensive training needed to build and oversee Canadian-based investment portfolios that include Canadian-traded securities.

All too often, clients are left holding their Canadian-dollar investment accounts in cash, simply because they cannot find a qualified financial professional based in the United States to expertly invest those assets.

OPTION 3 (the best option): Manage your cross-border investments with Cardinal Point.

The Cardinal Point difference is simple yet profound. We are legally registered to provide investment management and financial planning services in both Canada and the United States, without any restrictions or limitations. For clients who have investment accounts in both countries (RRSPs, IRAs, 401ks, Trusts, Non-Registered accounts, etc.), we construct integrated cross-border portfolios customized to each investor’s personal risk tolerance, needs, and goals.

Whether you are an individual living in the U.S. or are moving there with Canadian dollar investment accounts − or you have recently received a large sum of Canadian dollars from the sale of a home, business, or through inheritance, our fully certified Canada-U.S. portfolio management team can provide experienced and insightful help. We have the ability to invest your Canadian dollar accounts on a U.S. custodial platform and then tax-manage them based on your U.S. tax jurisdiction residency. As a U.S. resident partnering with Cardinal Point to oversee the management of your Canadian-dollar investment accounts, you gain significant benefits including:

- Fully compliant and customized U.S. tax reporting on Canadian-dollar investment assets

- Multi-currency investment accounts supported by a savvy investment team providing a variety of Canadian-dollar and U.S. dollar asset management services

- Flexible and convenient foreign exchange services

- Cardinal Point’s in-depth understanding of effective U.S. tax management strategies for Canadian-dollar investment accounts

- Additional cross-border financial, tax, and estate planning expertise for the sustained preservation and growth of your wealth

Please contact Cardinal Point to discuss your cross-border investment management, tax, retirement, and other financial planning needs.

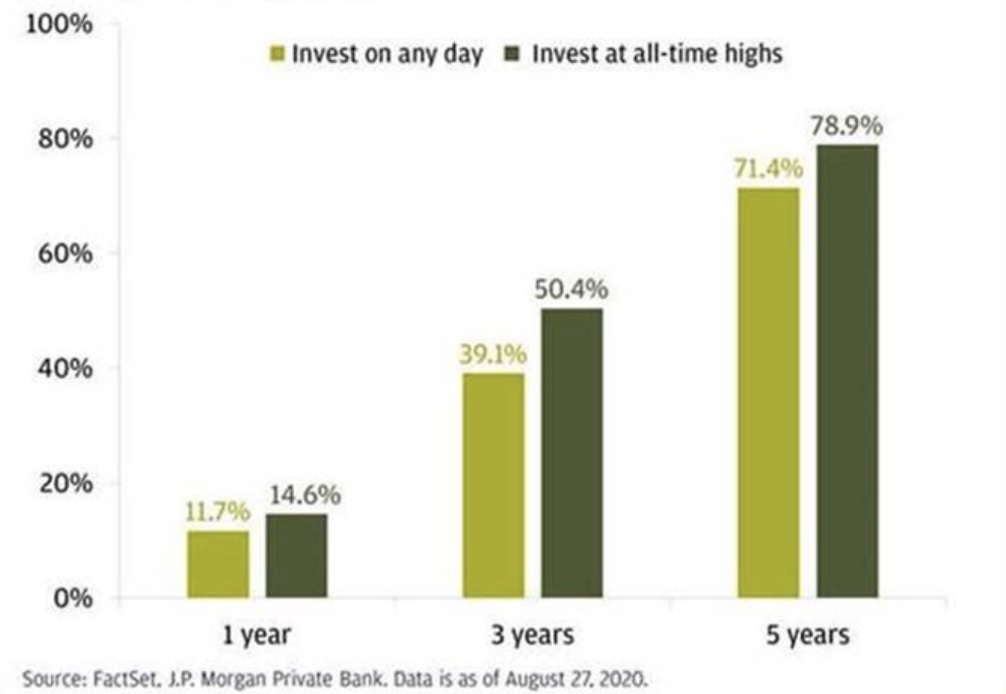

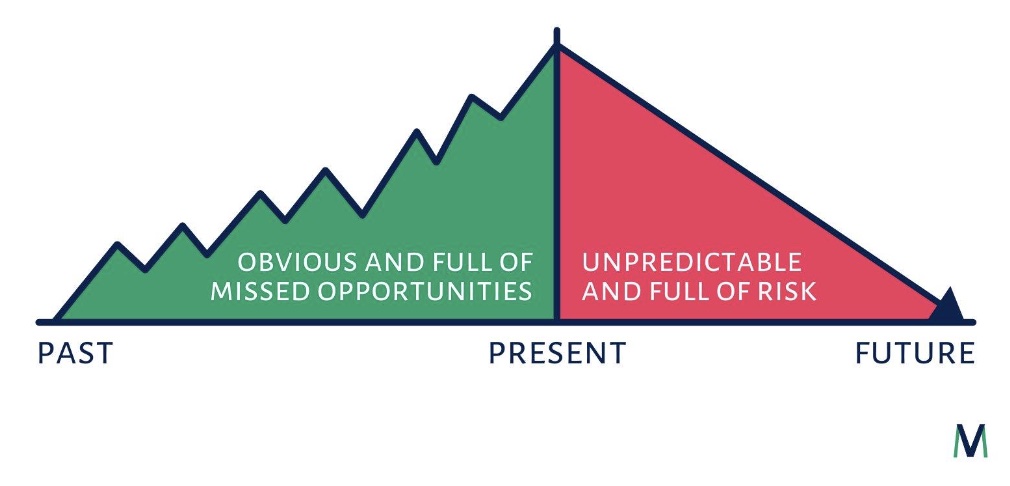

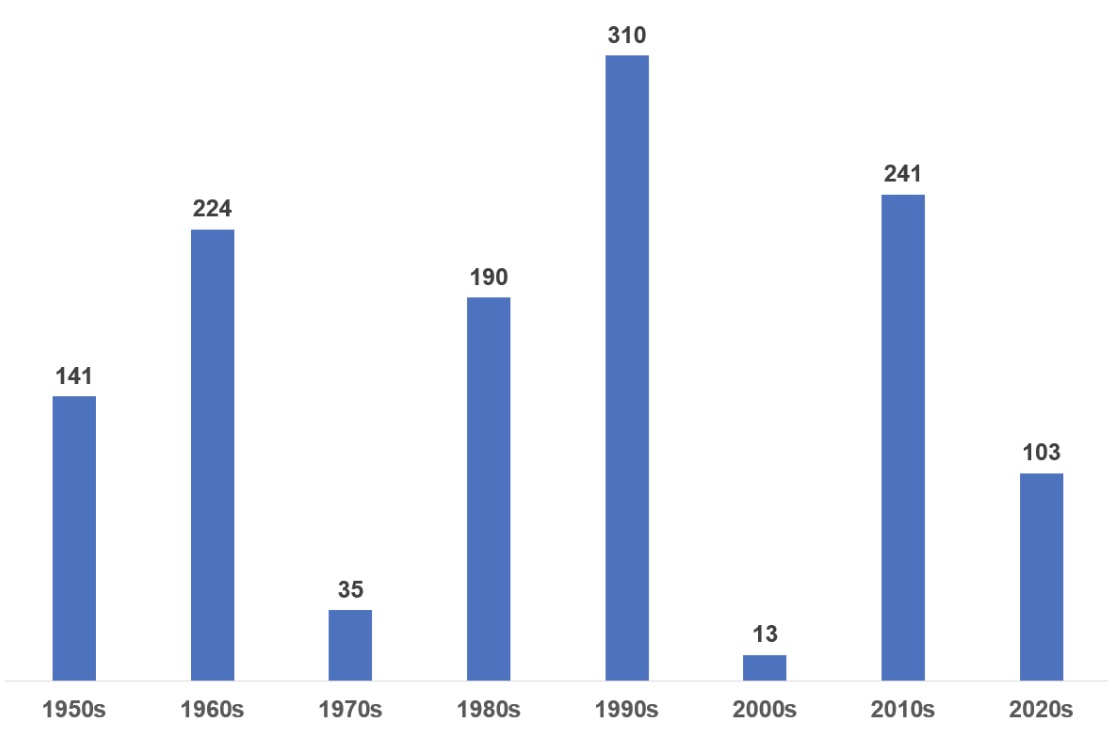

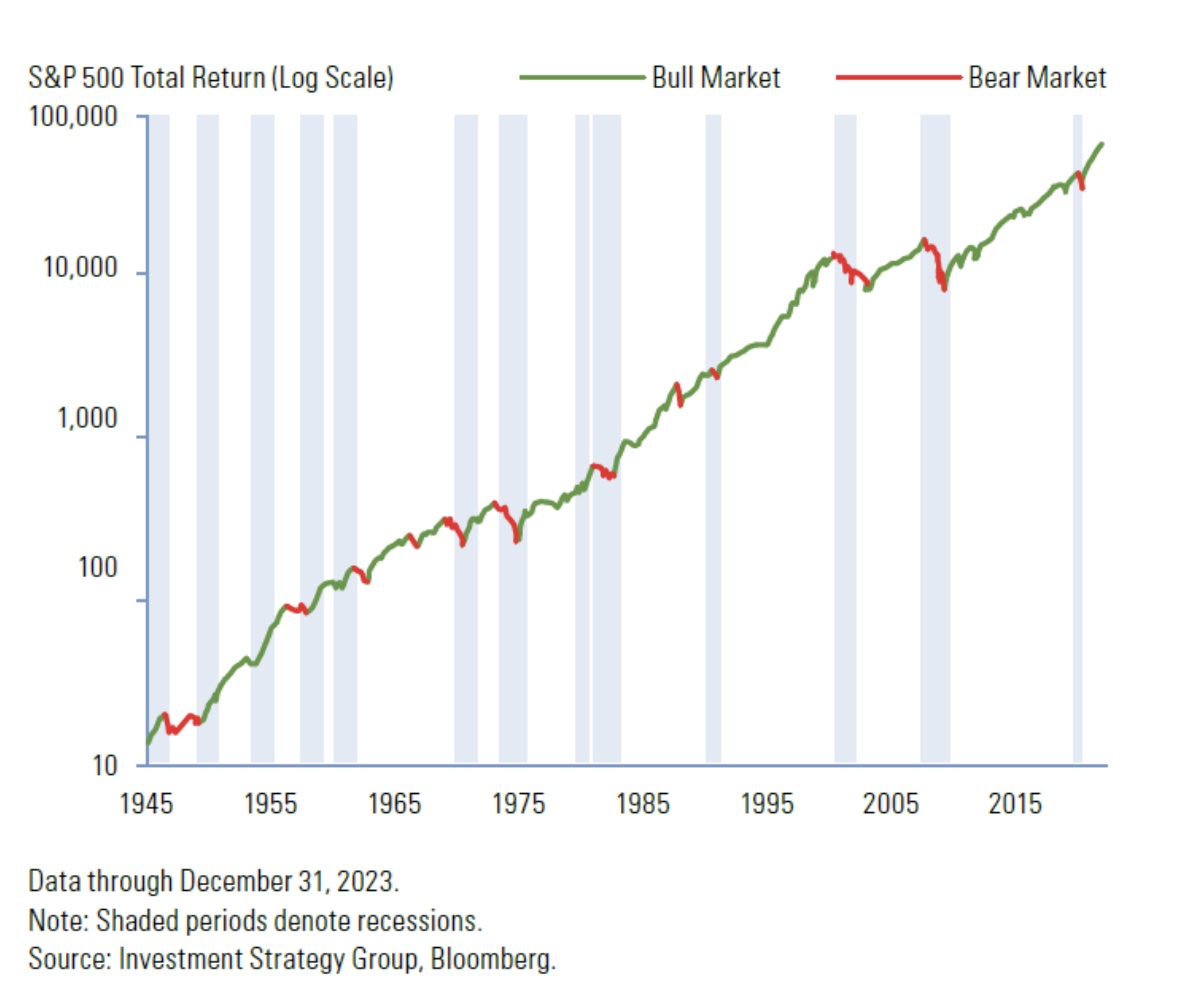

Using Bespoke Data we can look back at the S&P 500’s individual trading days since 1952, and see that the market has traded within 5% of its all-time high over 44% of the time. In other words, for almost half the market’s trading days the index was at (or very close to) its all-time highs. So that is a normal pattern, not an anomaly.

Using Bespoke Data we can look back at the S&P 500’s individual trading days since 1952, and see that the market has traded within 5% of its all-time high over 44% of the time. In other words, for almost half the market’s trading days the index was at (or very close to) its all-time highs. So that is a normal pattern, not an anomaly. But that raises a compelling question. New highs may be common, are investors really well-served when buying into the market at such lofty price points? The answer and the numbers may surprise you. The chart below from Creative Planning CEO Peter Mallouk compared 1, 3 and 5-year return when investing on any given day, versus when markets were at all-time highs.

But that raises a compelling question. New highs may be common, are investors really well-served when buying into the market at such lofty price points? The answer and the numbers may surprise you. The chart below from Creative Planning CEO Peter Mallouk compared 1, 3 and 5-year return when investing on any given day, versus when markets were at all-time highs.