CROSS-BORDER INVESTMENT MANAGEMENT RESOURCE HUB

The Cross-Border Investment Management Resource Hub is your go-to source for a wealth of valuable resources tailored to Americans and Canadians living, working, and retiring in Canada and the U.S. This comprehensive hub offers a diverse range of eBooks, infographics, videos, and articles, all from a U.S.-Canada perspective. Whether you’re seeking guidance on managing assets in both countries, understanding tax implications, or navigating cross-border investment strategies, our carefully curated content has you covered.

CROSS-BORDER INVESTMENT MANAGEMENT RESOURCE HUB

Discover the Cross-Border Investment Management Resource Hub, your go-to source for a wealth of valuable resources tailored to Americans and Canadians living, working, and retiring in Canada and the U.S. This comprehensive hub offers a diverse range of eBooks, infographics, videos, and articles, all from a U.S.-Canada perspective. Whether you’re seeking guidance on managing assets in both countries, understanding tax implications, or navigating cross-border investment strategies, our carefully curated content has you covered. Stay informed and make informed decisions with our invaluable resources, designed to empower you on your cross-border investment journey.

Stay informed and make informed decisions with our invaluable resources, designed to empower you on your cross-border investment journey.

CROSS-BORDER INVESTMENT MANAGEMENT EBOOKS

Explore our Cross-Border Investment Management eBooks, carefully crafted to bring clarity to the complexities of U.S.-Canada investment dynamics. Our eBooks dissect regulatory frameworks, tax implications, market trends, and strategic approaches, offering invaluable guidance for navigating cross-border investment landscapes. Whether you’re an American moving to Canada or Canadian moving the United States, our resources are tailored to help optimize your decision-making. Click below to access our latest eBooks.

Canadian residents: What are the tax implications in Canada and the U.S. when required to close a U.S. brokerage account?

New Ebook - Residents of Canada: What are the Canadian and U.S. Tax Ramifications when being forced to liquidate a U.S. brokerage account New enforcement of existing U.S. nonresident client regulations regarding U.S. taxable brokerage accounts means that many of these accounts are being forced to close, loosely based on the location of the primary [...]

Ebook: Cross Border Retirement Income: Canada Pension Plans, Canadian Old Age Security…

Those who have worked in both Canada and the U.S. may be eligible for Social Security (SS), Canada Pension Plan (CPP) and Canadian Old Age Security (OAS), but it can be complicated. While SS depends on years worked, OAS is based on years of Canadian residency, and CPP is based on contributions. You may be able to take early reduced benefits or delay them to receive increased payouts. There may be clawbacks based on income levels…

EBook: The Health Savings Account in a Canada-U.S. Context

A good savings or investment account allows you to avoid tax on contributions, income, and distribution. Not all available options meet these goals. For Americans living in the U.S., the Health Savings Account (HSA) does, in certain circumstances. For Americans living in Canada, though, the HSA’s benefits disappear as contributions cannot continue and tax liability opens up in Canada for income in the plan. Similarly for Canadians living in the U.S., benefits cease for Tax-Free Savings Accounts (TFSAs) and Registered Education Savings Plans (RESPs). Take a look at this e-book for more detail on the savings and investment plans available and see how they compare.

CROSS-BORDER INVESTMENT MANAGEMENT INFOGRAPHICS

Simplify Cross-Border Investment Management with Our Infographics. Our engaging visuals make the intricacies of Canada-U.S. investment strategies easy to understand. Whether you’re an American or Canadian living across the border, or planning to, our infographics break down complex investment concepts into clear, visual narratives.

Infographic: Lifetime Capital Gains Exemption & Qualified Small Business Corporation

The Lifetime Capital Gains Exemption (LCGE) is available to all Canadian residents and Americans living in Canada as a tax deduction on the sale of a Qualified Small Business Corporation (QSBC). It is indexed to inflation, and it can be used in part. Three tests must be met to claim an LCGE, and there are complicated regulations governing each of these.

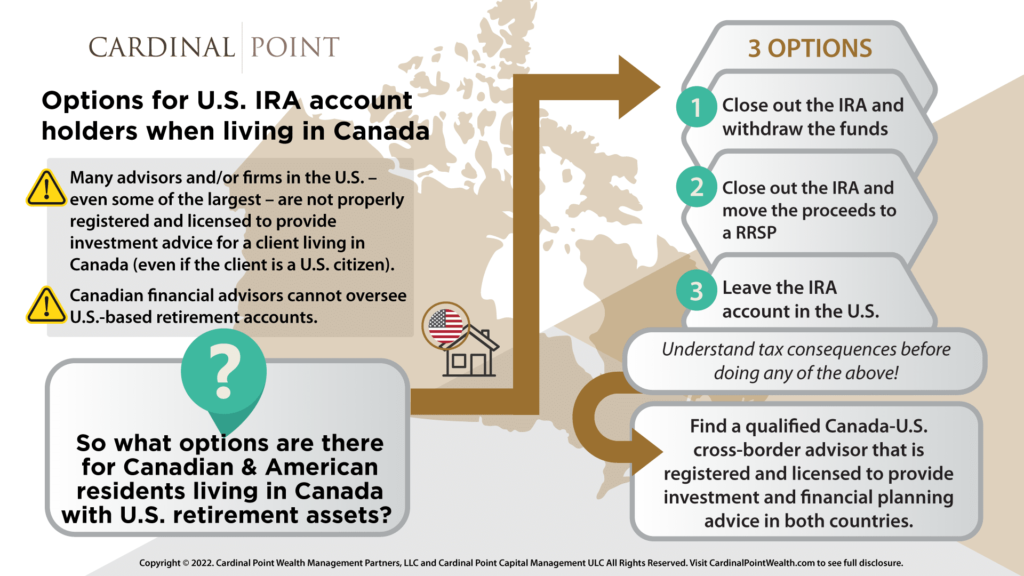

Infographic: Options for U.S. IRA account holders when living in Canada

Few financial advisors are licensed or equipped to provide investment advice for American and Canadian cross-border clients, and there is a lot of bad counsel circulating at present. The best advice usually leads to a choice from three main options, but which one?

CROSS-BORDER INVESTMENT MANAGEMENT VIDEOS

Discover our Cross-Border Investment Management Videos, created by the thought-leaders at Cardinal Point Wealth Management. These videos are designed to simplify the complex world of investing cross-border. They provide clear explanations of the laws, rules, and taxes that affect Canada-U.S. investments. Our specialists make complicated investment concepts easy to understand, giving you practical tips and insights. Whether you are already living as an expat, or preparing a transition, these videos will help you make smarter investment choices, and provide perspectives from Cross-Border Financial Advisors who have years of experience providing practical and timely insights.

Investment Basics for Americans in Canada

It’s a good idea for Americans living in Canada to understand which kinds of registered investment accounts they can have without having to confront onerous taxes and paperwork. Two kinds of plans are friendliest for Americans: The Registered Retirement Savings Plan (RRSP) and the Registered Retirement Income Fund (RRIF). Effectively, U.S. citizens are simply taxed […]

How US PFIC Rules Can Impact Your Clients

Cardinal Point’s Terry Ritchie discusses the impact of U.S. PFIC (Passive Foreign Investment Company) tax rules on U.S. citizens living in Canada who hold Canadian mutual funds or ETFs. The challenge is that under U.S. tax law, the earnings and dividends from these PFICs are not taxed the same way in the U.S. as they […]

CROSS-BORDER INVESTMENT MANAGEMENT BLOGS

Our Cross-Border Investment Management Blog is a premier source of expertise and insight for Canadians and Americans navigating the complexities of living, working, retiring, or enjoying the snowbird lifestyle across borders. Crafted by a distinguished team of cardinal point thought leaders, seasoned authors, and dedicated contributors, our articles serve as a comprehensive guide to the myriad rules, regulations, and tax laws influencing cross-border financial planning. Each piece is designed to educate and foster awareness, offering valuable tips, tactics, strategies, and advice on a wide range of timely topics. Our goal is to empower our readers with the knowledge they need to make informed decisions and optimize their cross-border lifestyle.

Moving from Canada to the U.S.: What to do with your Canadian dollar investments

Anyone planning to move from Canada to the United States, or who has already made that move, must give careful consideration to how they manage their Canadian dollar denominated investments. Otherwise they risk consequences such as having those investment accounts frozen or discovering that their Canadian-based financial professionals are prohibited from managing their investments once they become U.S. residents. But to make matters even more complicated, they may be unable to find a qualified financial and tax advisor in the United States to manage their Canadian dollar assets. The good news is that you have viable options and excellent solutions to help you avoid these and other unwanted and costly scenarios. All of that is explained in this highly informative and helpful blog.

Should I Buy Stocks at All-Time Highs?

Conventional wisdom tells us that it’s always best to “buy low, sell high.” But contrary to what most investors may realize, decades of S&P 500 data confirms that record highs are rather commonplace – and investing when the stock market is at, or close to, those highs may deliver significantly positive returns. In fact, buying into the market during those historic upticks may generate investor gains that are actually greater than the ones achieved by those who invest at all other times. This phenomenon may sound quite contrary to typical investment logic. But as this blog explains, there is plenty of factual evidence to support the idea that buying high (even in years like 2024 when there’s the uncertainty of a U.S. presidential election) may be a sound long-term strategy for achieving your financial goals.

Cross-Border Wealth Management: Overcoming the Downside of Over-Funding Your Child’s 529 Plan

For both Canadian and U.S. residents, a 529 plan can be a very effective tool to help save for a child’s higher education. Plus, recently passed U.S. legislation under the SECURE Act 2.0 offers a unique way to more efficiently manage 529 contributions. Starting in 2024, it will be possible to transfer into a Roth IRA any extra funds that remain in the 529 after all educational expenses have been paid – as long as certain eligibility requirements are met. As this blog explains, that can enable you to avoid steep 529 withdrawal taxes and penalties, while continuing to accumulate wealth in a tax-free Roth IRA.

Cross Border Wealth Management: Navigating your RESP

A Registered Education Savings Plan (RESP) is a powerful asset when saving to pay for post-secondary education. College tuition had already become almost prohibitively expensive, years before recent historic inflationary pressures made the cost of higher education rise even more dramatically. That’s a constant challenge for parents who want to help fund their children’s post-secondary education. Navigating those challenges becomes more complicated when the RESP subscriber or the beneficiary reside in different countries. This article gives you an informative overview of some of the most common challenges, and insight into the most effective ways to proactively manage an RESP as part of your cross-border tax and financial planning.

The ABCs of RCAs

In eight Canadian provinces, people in the top tax bracket are subject to tax rates of over 50%, while those in the other two provinces pay 47.5% (or more). However, high income earners can save substantial amounts of retirement income by utilizing a lesser known strategy involving Retirement Compensation Arrangements (RCA). Those who can potentially benefit the most from this strategy include highly paid executives and business owners (or others such as professional athletes) whose compensation is tied to special incentives. Setting up an RCA is a rather complicated process, but the benefits are well worth it for those who are eligible – and can result in many thousands of dollars extra per year in retirement. Read the ABCs of RCAs blog for a detailed explanation of how to take advantage of this unique tax-saving approach to wealth management.

Fiduciary Standard or a Pretender

A Cardinal Point advisor adheres rigorously to the fiduciary standard—a commitment that puts your interests ahead of those of Cardinal Point or any outside organization. Some financial advisors do not; instead, they skew their advice and investment options to ones which benefit them. For Cardinal Point clients, it is most reassuring to know that all recommendations must be made with only one concern: that this is the best thing for you.

Secure Act 2.0: What You Need To Know

There are a number of rules changes proposed by Congress that will impact retirement accounts. The changes will benefit US residents and also Canadians with IRAs and other retirement accounts. There are many ways this could be advantageous for you, possibly deferring tax or extending benefits. Cardinal Point, as the leading cross-border specialist, can show you how.

Cross-Border Financial Planning: Currency Conversion Considerations

While currency exchange is not recommended for speculation, many clients will need a different currency in the future. For them, fluctuations in currency exchange markets create opportunities to time conversions that need to be made eventually. However, there are numerous factors to consider beforehand, such as when the need will be, capital gains tax questions, historical averages, conversion costs, and availability of investment opportunities.

Update on Required Minimum Distributions

Good news on the tax front as the IRS lengthens life expectancies for its RMDs. The result of this may be an effective tax cut for you. If you are a US citizen or expat living in Canada, Cardinal Point Wealth Management can assist with complicated cross-border financial and tax planning.

How Much Risk is There in Bonds?

With recent headlines touting hidden bond risks, you may be wondering if you should be concerned about your bond holdings. In this piece we’ll take a look at why Cardinal Point views bonds as a means to provide stability in client portfolios and not an area of dramatic long-term risk.

Environmental, Social, and Corporate Governance Investing

Would you like to align your investments with your personal views? If so, ESG investing—also known as socially responsible investing or impact investing—may be for you. In this blog post, we’ll take a brief look at recent growth in this investing model as well as the various factors evaluated within it.

Hedging Currency in Your Portfolio: Strategies & Insights

Do you have assets in two or more countries? If so, you’ll want to read this blog post about managing the different currencies in your portfolio. In it, you’ll learn more about Cardinal Point’s philosophy on currency hedging including considering your future income needs.

Retirement Compensation Arrangements: Are They Right For You?

Navigating Retirement Planning: Evaluating the Suitability of Retirement Compensation Arrangements A Retirement Compensation arrangement is perhaps the most effective and misunderstood tax deferment opportunity that exists in Canada today. It may be used for a wide range of situations, including small business owners, athletes, incorporated professionals, highly paid executives receiving yearly bonuses, and those approaching […]

Why Invest Internationally? | Cardinal Point Wealth

Diversification is the most important concept in investing, but also perhaps the least exciting. If anyone knew for sure exactly which one company or country would have the highest return in the coming year,- there would be no reason to hold anything else. But while being able to predict markets with any certainty sounds great in theory,- in practice nobody has been able to consistently outsmart the market. So what do you do if you can’t predict be the best performing stock or sector in the coming year? You diversify.

Don’t Settle: Choose wisely when selecting a cross-border wealth management firm

Your whole life you have done things correctly: worked hard, saved and prudently invested your money. Then one day, out of the blue, you receive a letter from your U.S. investment management firm saying they no longer want to work with you because you reside outside of the U.S. Worse yet, they give you 90 […]