[player id=1446]

Snap Projections, a financial planning software company, recently featured Cardinal Point’s Partner and Director of Cross Border Wealth Services, Terry Ritchie, on their Growing Your Financial Advisory Practice podcast. Given Terry’s more than 30 years of experience in cross-border financial, investment, tax, and estate planning, it’s no surprise that Snap Projections chose to tap into his insight for this primer directed at financial planners who want to serve US-Canada clients.

From the factors driving clients to move between Canada and the US (hint: politics, healthcare, family, and lifestyle all play a role) to the intricacies of visas, green cards, and US income tax, the podcast highlights Terry’s wealth of knowledge and passion for cross-border work.

Here’s everything discussed in the one-hour episode:

- Why people move between Canada and the US.

- Why Terry thinks cross-border work matters.

- What you MUST know about visas and green cards.

- Important elements of US income tax.

- Limitations on Canadians who invest in the US.

- Estate planning for cross-border clients.

- The biggest cross-border planning mistake advisors make.

- How to grow a financial planning career you really love.

Last month we took a family trip to the Oakland zoo with our two young children. The following is a picture of my 2 year old son turning a key into the same recording box at the Giraffe exhibit that I wished I could have all those years back.

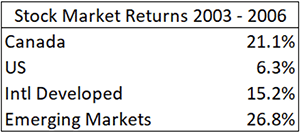

Last month we took a family trip to the Oakland zoo with our two young children. The following is a picture of my 2 year old son turning a key into the same recording box at the Giraffe exhibit that I wished I could have all those years back. Let’s take an example of a Canadian investor who had a CAD account and was watching returns in the early 2000s. Between the start of 2003 and the end of 2006, the Canadian market far outpaced the US. You can see from the chart on the left that the annualized returns (in CAD) for Canadian markets was nearly triple the returns for US markets over that period.

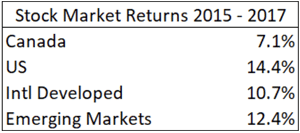

Let’s take an example of a Canadian investor who had a CAD account and was watching returns in the early 2000s. Between the start of 2003 and the end of 2006, the Canadian market far outpaced the US. You can see from the chart on the left that the annualized returns (in CAD) for Canadian markets was nearly triple the returns for US markets over that period. More recently, if we look at 2015-2017, Canada has delivered just half the performance of the US on an annualized basis, and well below the returns experienced in International Developed and Emerging Markets.

More recently, if we look at 2015-2017, Canada has delivered just half the performance of the US on an annualized basis, and well below the returns experienced in International Developed and Emerging Markets.